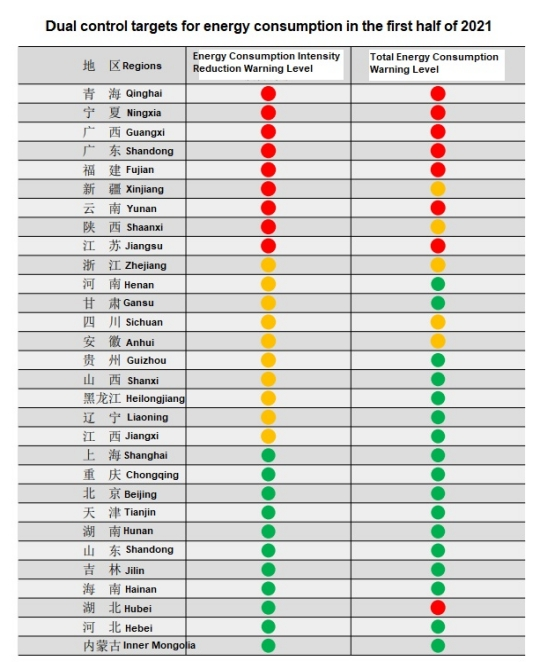

On August 12, 2021, the National Development and Reform Commission issued The Barometer of Target Achievement. In which the reduction of energy intensity, Ningxia, Qinghai, Ningxia, Guangxi, Guangdong, Fujian, Xinjiang, Yunnan, Shaanxi, Jiangsu 9 provinces (autonomous District) the energy consumption intensity has risen instead of falling in the first half of 2021.

Therefore, the energy consumption intensity of the above 9 provinces (autonomous regions) reduce to one level, and suspend the review of the "two highs" project in 2021. At the same time, the "Barometer" also requires each province (autonomous regions) should take favorable measures to ensure the completion of the annual energy consumption double control target, especially the reduction of energy consumption intensity. Low goal tasks.

Red is a first-level warning, and the form of expression is very severe; orange is a second-level warning, and the form of expression is relatively severe; green is a three-level warning, indicating that progress is generally smooth.

We can learn from the chart above that most of the vitamin industry is located in Zhejiang, Jiangsu, Shandong, Jiangxi and other places.

However, it is another 35 kinds of chemicals that have been affected rather than vitamins. They are including pesticides, potassium chloride, yellow phosphors, phosphorus trichloride, glyphosate, titanium dioxide, phosphorus, fluorine, caustic soda, lithium hexafluorophosphate, phosphoric acid, Silicone, trichloroethylene, etc.

Relatively speaking, due to the scale of electricity consumption, power and coal restrictions have little impact. In recent years, the overall supply of the vitamin market has exceeded demand. As far as the current situation is concerned, the fundamentals of this market have not fundamentally changed.

Due to the continuous strengthening of the dual control policy again, the operating rate of some factories is limited. The production companies that have been clearly affected by the operating rate include: Nanjing Bluestar Adisseo (hydroxymethionine), CUC (DL-methionine), Tongliao Meihua (L-threonine), Chengfu (L-threonine). Among them, Chengfu’s L-threonine production was discontinued, CUC’s methionine production was limited to 50%, and a certain L-threonine production capacity in Inner Mongolia was also limited by 40-50%. Currently, the legendary restricted NHU amino acids (DL-methionine), Inner Mongolia EPPEN (L-lysine and L-threonine), Heilongjiang Daqing (L-lysine and L-threonine) And Northeast Fufeng (L-threonine) and Qiqihar Fufeng (L-lysine and L-threonine) have not actually started to limit production, but the production enterprises in Inner Mongolia and Heilongjiang have received relevant departments Announcement of production restriction/discontinuation of production, therefore, there is a risk of production restriction and discontinuation at any time in the next few weeks.

In the past 10 days, different market influencing factors have continued to produce and ferment. Whether it is the amino acid market or the vitamin market, it can be said to be chaotic. The main theme is price increases. Both manufacturers and buyers have begun to lose sight of this market. More essence and truth behind it. Electricity curtailment, coal restrictions, and coal prices have risen sharply. This should be the black swan of this chaos.

On October 10, the PPI Thermal Coal Commodity Index was 237.95, a record high in the cycle. It was an increase of 432% from the lowest point of 45 on January 20, 2016, and an increase of 99.0% from July (Data source: Business News). In addition to the real impact of this wave of bulk raw material growth on the growth of vitamin and amino acid production costs, the impact on the psychology of the market masses has also been multiplied.

| Raw material | Price raise after July 2021 | Related products |

| Liquid ammonia | 12% | Almost all the amino acids and vitamins. Bigger impact in Amino acids |

| Sulfuric acid | 35% | Almost all the amino acids and vitamins. Bigger impact in Amino acids |

| Acetone | 30% | Vitamins, especially Vitamin E and D3 |

| Natural Gas | 36% | DL-Methionine |

| Sulphur | 19% | DL-methionine |

| Propylene | 21% | DL-methionine |

| Calcium carbide | 65% | Kinds of vitamins |

The direct impact on amino acids and vitamins is the increase in power costs. Taking the average consumption of 2 tons of thermal coal per ton of fermented amino acid as an example, the power cost per ton of product has increased by 400-600 yuan/ton.

Therefore, the impact of "dual control", "power curtailment" and coal price hikes on the amino acid and vitamin industries will continue, but the impact may not be as great as everyone's sudden feelings.

Based on the information obtained from different channels, this wave of dual control policies, electricity and coal restrictions, and coal price increases are expected to last until the first half of 2022.

Source:

SUBSCRIBE

NOW

Uganda

Uganda

India

India

Indonesia

Indonesia

Malaysia

Malaysia

Myanmar

Myanmar

Philippines

Philippines

Taiwan

Taiwan

Thailand

Thailand

Vietnam

Vietnam

Australia

Australia

New Zealand

New Zealand

Uganda

Uganda

India

India

Indonesia

Indonesia

Malaysia

Malaysia

Myanmar

Myanmar

Philippines

Philippines

Taiwan

Taiwan

Thailand

Thailand

Vietnam

Vietnam

Australia

Australia

New Zealand

New Zealand